The Capital Cycle

I just finished reading Capital Returns: Investing Through the Capital Cycle by Edward Chancellor. It was one of the best investing books I've read in a while, so I highly recommend it!

The book is a collection of sixty of the most insightful reports written by portfolio managers at Marathon Asset Management, a London-based firm managing over $50 billion of assets.

The book centers around capital cycle analysis to understand and profit from boom-and-bust cycles in various industries.

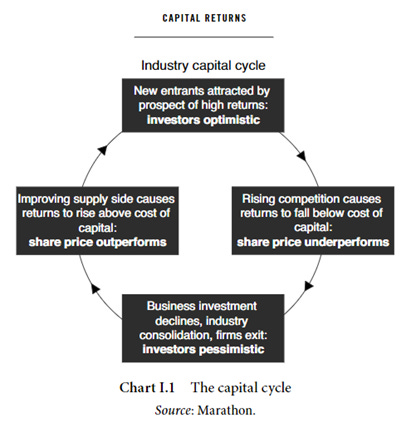

Here’s what the typical capital cycle looks like according to Marathon:

The book's primary premise is that investors considering investing in an industry should not focus on understanding the demand picture. They should focus on the supply picture. An industry where the supply of products is increasing or can increase rapidly can ruin the economic benefits for all the players involved, regardless of the market demand.

‘‘Long-range demand projections are likely to result in large forecasting errors. Capital cycle analysis, however, focuses on supply rather than demand. Supply prospects are far less uncertain than demand, and thus easier to forecast. In fact, increases in an industry’s aggregate supply are often well flagged and come with varying lags […]’’

The easiest way to think about the supply dynamics is to picture the two extremes, boom and bust.

The boom phase has the following characteristics:

An industry’s demand picture is attractive or improving, leading to optimism by company executives to invest in expanding production capacity (supply).

Investors are also optimistic about the industry’s prospects and are willing to provide capital for the expansion phase.

Share prices and valuations increase, leading to more willingness to invest.

New players enter the industry at a rapid pace.

Industry fragmentation and competition increase.

There is a wave of new IPOs, secondary offerings and debt issuances.

All of these factors lead to the supply massively overshooting demand and eroding the returns for everyone.

On the other end of the spectrum, the bust phase has the following characteristics:

The demand picture turns out to have been overstated, or the supply picture is so bad that nobody is willing to invest in new production capacity.

Investors are pessimistic and not willing to provide any new capital.

Share prices and valuations crater, reducing willingness to invest.

Profitability is low or non-existent.

There is a wave of bankruptcies as excess capacity exits the industry.

The industry consolidates, and competition decreases.

Ultimately, the few remaining players learn to cooperate and exercise ‘‘pricing discipline,’’ leading to improved economic returns.

Some of the best investment opportunities can be found at the end of the bust phase, when the economics of an industry start to improve but valuations remain at trough levels.

One of the best examples that comes to mind is the current Canadian cannabis industry. Think back to the 2017-2019 bubble when massive amounts of capital were invested to build cultivation capacity, leading to a gigantic market oversupply. The industry has worked through this oversupply problem for the last five years.

If you read my bullet points about the bust phase again, you’ll notice an awful lot of similarities with the current picture in the Canadian cannabis industry. Barely any new capital has entered this industry in the last several years. Share prices have cratered. Profitability is almost non-existent, except for a few outliers like Cannara Biotech (TSX-V: LOVE). According to a court filing, 66 cannabis companies have entered insolvency proceedings in Canada during the last three years. Some major players started consolidating, like the Motif Labs acquisition by Organigram Global (TSX: OGI) in December 2024.

It's clear that the industry economics are now improving, but nobody’s paying attention… yet. Why? Because an industry with no supply expansion isn’t profitable for the capital providers. Nobody’s raising money.

The Role of the Finance Industry

Marathon portfolio managers highlight an essential point in the book about the involvement of industry participants, specifically the investment banks.

The role of the investment bank is ‘‘to supply finance to capital-hungry businesses – for which they earn generous fees.’’ They are essentially paid to drive capital cycles. They make money on the way up by raising massive amounts of capital for companies, and on the way down by advising on mergers and acquisitions opportunities when the inevitable consolidation happens.

I’m not saying that investment banks are bad actors. They serve an essential function in today’s capital markets. They help many deserving companies raise capital for the right reasons and projects.

However, when you understand their motivations and incentives, the industries they’re most active in, and the types of companies their analysts cover, you gain some perspective on the state of the capital cycle in different sectors. If you’re investing with a long-term view, you want to avoid the so-called ‘‘hot sectors’’ that everybody pays attention to and where supply is rapidly increasing.

A Word on Management

The ability for an individual company to navigate and profit from the capital cycle is highly reliant on management. You want to identify a management team that will adopt a counter-cyclical attitude. They must be prudent with expansion during the boom phase (and perhaps sell assets) while turning aggressive on M&A opportunities and share buybacks during the bust phase.

‘‘Marathon looks to invest with corporate managers who know how to allocate capital effectively. This requires certain character traits in the individual, such as suspicion of investments fads (and investment bankers), and a willingness to swim against the tide. […]

We go into meetings looking for answers to questions such as: does the CEO think in a long-term strategic way about the business? Understand how the capital cycle operates in their industry? Seem intelligent, energetic and passionate about the business? And interact with colleagues and others in an encouraging way? Appear trustworthy and honest? Act in a shareholder-friendly way even down to the smallest detail?’’

When you invest with a long-term view, answering these questions is way more relevant than understanding the outlook for the next quarter or two. That’s why I almost always speak with management teams (several times) before investing and why I like to visit companies in person. You can gain a deeper understanding of a company’s culture and how management behaves when you do this type of work.

What About Growth Stocks?

If you’ve made it this far, you might think that an investment strategy based on capital cycle analysis is one where you only look at washed-out industries with stocks trading near 52-week lows.

That’s not the case.

You can also use the capital cycle framework to identify industries where companies are insulated from supply-side shifts. In finance, most things tend to mean-revert. Money and talent gravitate to industries where unusually high profits can be earned, increasing competition and eroding returns over time. High profitability is competed away.

Identify an industry where it is incredibly challenging to increase supply due to high barriers to entry, and you might find a company that can earn high profits for years or even decades.

“Companies with such strong competitive advantages, possessing what Warren Buffett calls a wide “moat,” are able to maintain profits, often for longer than the market expects. Mean reversion is suspended. From a capital cycle perspective, it can be observed that a lack of competition prevents the supply side from shifting in response to high profitability.’’

Overall, I thought the book's concepts could apply to various investment strategies.

It was a fascinating read and one I will probably revisit once every few years.

I highlighted the Canadian cannabis industry as the prime candidate I’m seeing to apply the capital cycle analysis concepts. Still, I’m sure there are other areas of the market where opportunities exist.

Which opportunities are you seeing and why? Please comment and let me know!

Disclaimer

This publication is for informational purposes only. Nothing produced under the Stocks & Stones brand should be construed as investment advice or recommendations. Mathieu Martin, the author, is employed as a Portfolio Manager with Rivemont Investments. This publication only represents Mathieu Martin’s own opinions and not those of Rivemont. Rivemont may own positions and transact on any securities mentioned in this publication at any time without prior notice. At the time of this writing, the Rivemont MicroCap Fund holds shares of Cannara Biotech (TSX-V: LOVE). Always do your own research and consult a professional before making investment decisions.

If you’d like to invest in small public companies, check out this post.

Hi Mathieu , great write-up. Capital Returns is hands down my favourite investment book too. It goes well beyond the usual finance blah blah. Analyzing competitive dynamics is something most investors overlook. It’s hard work and doesn’t offer immediate answers, but in my view, it’s essential for generating long-term outperformance.